The first of our strategies is the use of the relative strength index (RSI) in buying undervalued stocks. As Investopedia explain "The RSI is a technical momentum indicator that compares the magnitude of recent gains to recent losses in an attempt to determine overbought and oversold conditions of an asset. It is calculated using the following formula:

RSI = 100 - 100/(1 + RS*)

*Where RS = Average of x days' up closes / Average of x days' down closes.

Most people deem an RSI approaching 30 (or below) to be oversold, meaning that the stock may now start an uptrend, and an RSI approaching 70 (or above) to be overbought, causing the asset to start a downtrend.

Our approach

So, for this investigation we are going to look at the what if scenario for the portfolio performance if buying all stocks approaching an RSI of 30, as well as a specially selected group of stocks approaching an RSI of 30 that satisfy a few fundamental factors.

As of October 25 2014 we have 703 stocks that are approaching an RSI of 30. For the purpose of this experiment we are going to class 'approaching an RSI of 30' as any stock below an RSI of 40 on 14 day basis.

We have placed all 703 stocks in an equally-weighted portfolio together and will track them for one month, removing individual stocks from the study as they approach an RSI of 70 and thus are categorised as being overbought. At the end of the month we will judge the portfolio against the market performance and other portfolios within the study.

The special selection

Sometimes there are fundamental reasons why a stock is trading with a low RSI. A company that is heading to bankruptcy, for example, would see very little buying when heading to $0.

So for this reason we have screened through our data for stocks with fundamentally strong features that may greater encourage a change in momentum.

The follow criterion had to be satisfied to be included in this particular portfolio.

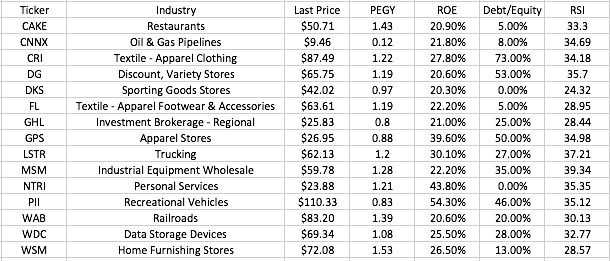

- Return on Equity > 20%

- Debt to Equity < 80%

- PEGY Ratio < 2

- Relative Strength Index < 40

Out of over 7000 stocks we were left with just 15 stocks that satisfied our criterion. These stocks were:

Once again these stocks will be held for one month, or until they approach an RSI of 70 and thus are categorised as being overbought.

Finally - for the purists.

Some people prefer to class oversold as strictly below an RSI of 30. For this reason, a third portfolio has been constructed containing 148 stocks that currently trade with an RSI below 30. The same rules apply for this portfolio.

We will report back with regular updates as we investigate this trading strategy.

- J